Housing and Transit Reinvestment Zones (HTRZ)

Open: Ongoing

Expires: December 31, 2027

In the 2021 General Legislative Session, the Housing and Transit Reinvestment Zone Act (SB 217) was adopted and allows for a municipality or a public transit county to propose a Housing and Transit Reinvestment Zone, or HTRZ, around strategic transit stations along the Wasatch Front.

An HTRZ is a strategic tool that enables a portion of incremental tax revenue growth to be captured over a period of time to support costs of development. The bill has been amended in subsequent years to expand eligibility to different types of transit, limit the number of allowable HTRZs, change committee membership, and provide additional clarification.

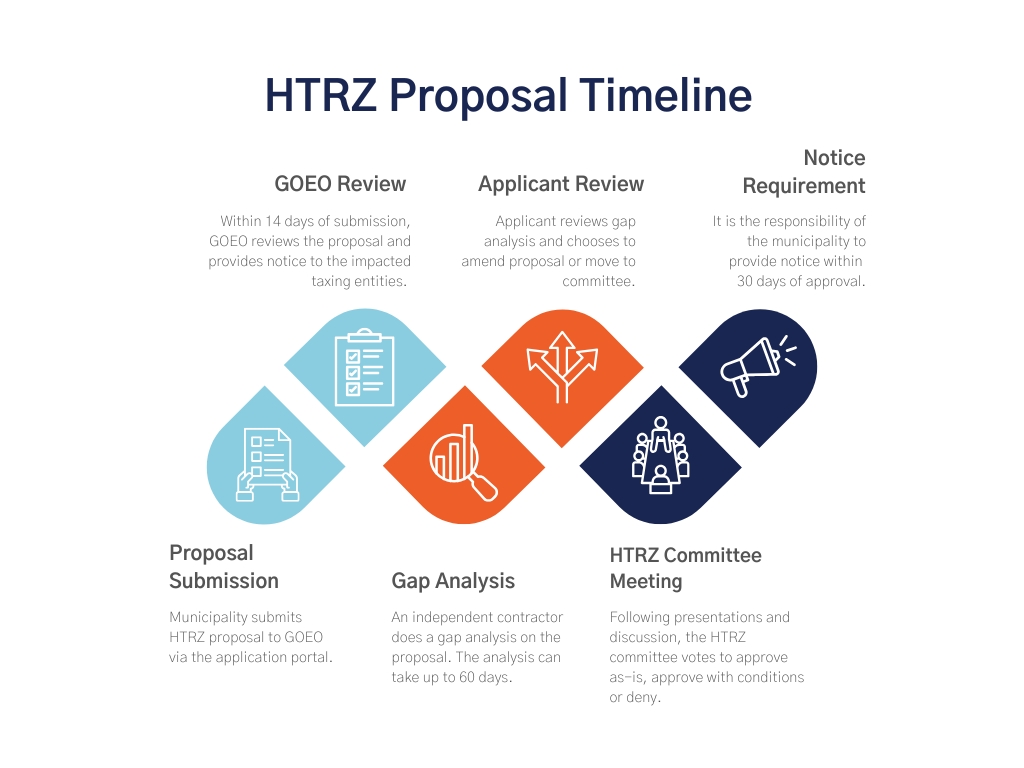

To request access to the HTRZ application portal or for additional information on HTRZ, interested municipalities or public transit counties should contact the office at [email protected].

Updates from the 2026 Legislative Session

H.B. 507: State Coordination of Regional and Local Economic Development Projects Amendments

- Sunset Provision: Establishes December 31, 2027, as the termination date for HTRZs

- Radius Restrictions: Clarifies requirements for zones that incorporate two to three transit stations

- Extraterritorial Affordable Housing: Authorizes the use of HTRZ funds for affordable housing located outside the HTRZ but within city boundaries, provided the project benefits the HTRZ. Qualifying housing must:

- Be affordable

- Maintain a density of at least six units per acre

- Be owner-occupied for at least 25 years

S.B. 39: Investment Zones Amendments

- Administrative Transfer: Relocates HTRZ provisions to the Housing Investment and Opportunity Act (63N Chapter 23) under the Governor's Office of Economic Development (GOED).

- Standardization: Establishes consistent definitions for "base taxable value" and "incremental value" across all Tax Increment Financing (TIF) projects

S.B. 206: Tax Amendments

- STATS Program: Creates the Statewide Tax Administration and Technology Solutions (STATS) program.

- Reporting Requirements:

- Mandates that any TIF entity intending to utilize tax increments must complete pre-increment disclosure and reporting.

- Requires TIF recipients to submit ongoing, annual tax increment receipt reports to the STATS program.